This is the fourth piece in my series on the 2025 AI Index Report.

This is where AI moves from lab demos to the real world. The data covers how companies are hiring, where they're deploying AI, and what kinds of bets investors are making to stay ahead.

This article looks at two sides of that transformation:

What AI is doing to jobs and corporate strategy: who's hiring, who's replacing, and how companies are reshaping operations. Where capital is flowing, and what that says about the infrastructure quietly forming under all those shiny model releases.

Let's get into it.

1. Labor and Companies

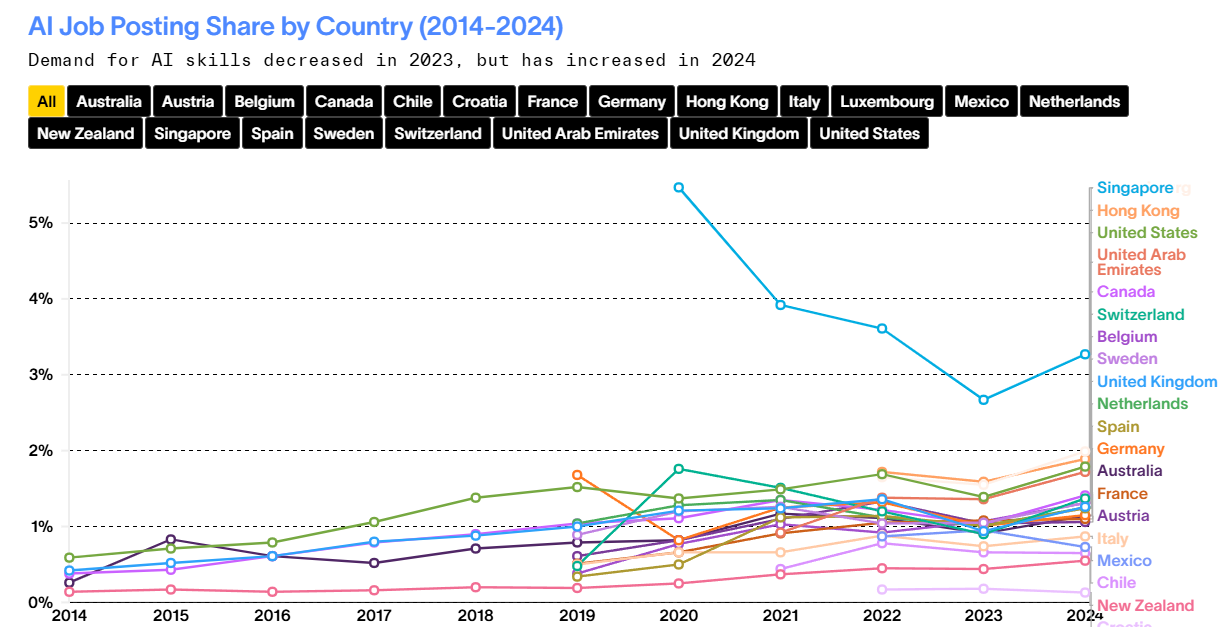

AI Skill Demand On the Rise

In 2024, the percentage of global job postings requiring AI-related skills increased across the board. Leading the pack was Singapore, where 3.3% of all listings included AI skills, well ahead of most advanced economies.

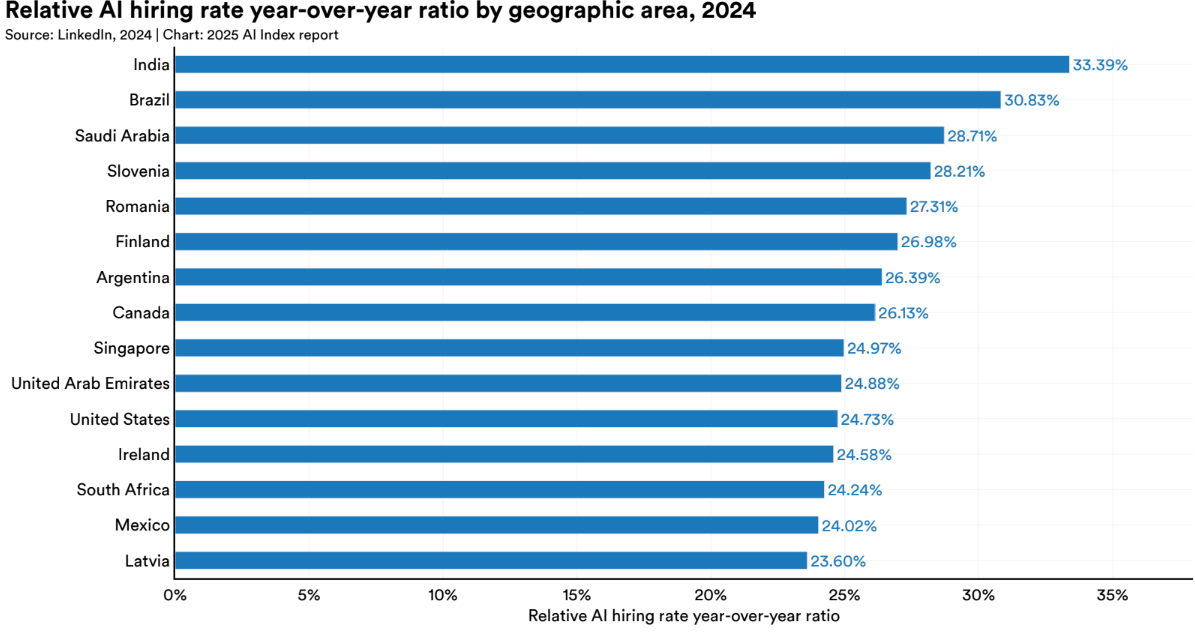

Meanwhile, fast-growing economies are rapidly expanding their AI footprint. India recorded the highest relative increase in AI hiring in 2024, followed by Brazil and Saudi Arabia.

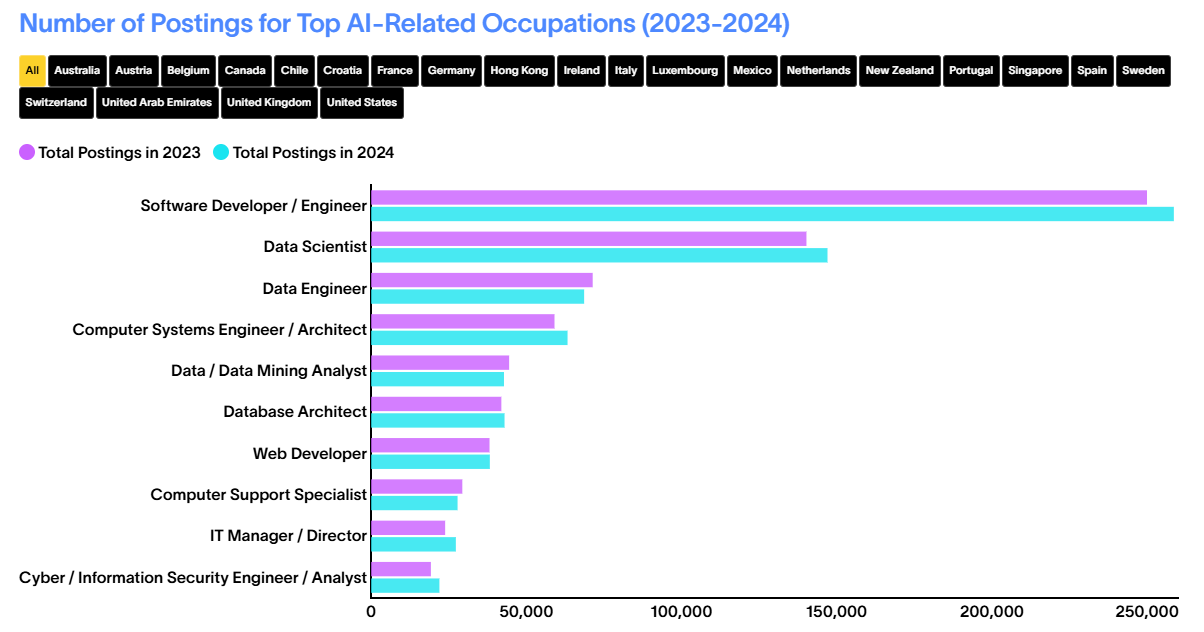

The Roles in Demand

AI hiring is concentrating around a familiar core. According to the data, the most in-demand AI-related roles in 2024 were:

Software developers and engineers, by a wide margin. Data scientists. Data engineers. Followed by computer systems architects, database specialists, and cybersecurity analysts.

These aren't new roles, but they're scaling fast. Software development alone accounted for nearly 250,000 postings, with year-over-year growth visible across nearly every role on the list. The message is clear: AI is still focused on technical jobs, and pulling related professions (like security, analytics, and systems architecture) into the spotlight. Companies want AI-literate professionals in core operational roles.

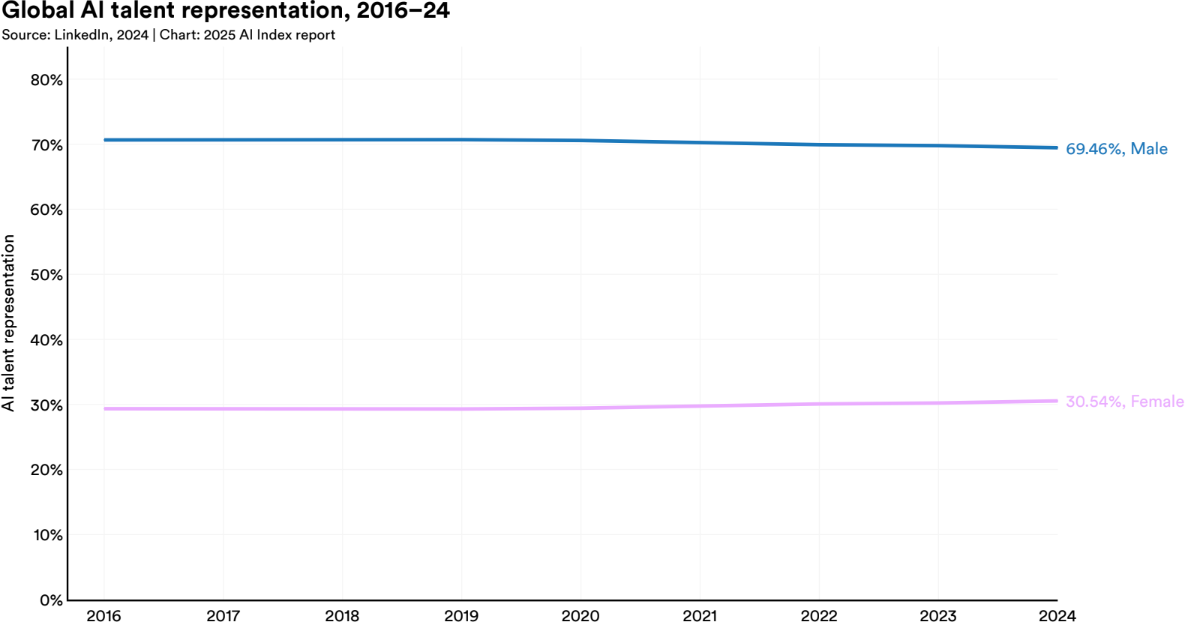

Gender Gaps

In 2024, men still made up a hefty 69.5% of all AI talent globally, according to LinkedIn. Women represented just 30.5%. What's more striking? This number hasn't budged much over the past several years.

The gap is consistent across nearly all countries. Even in places with strong AI ecosystems, like Germany, the U.S., France or the U.K., women remain significantly underrepresented. Only Romania comes close to parity with a 59%-41% split.

Across countries, significantly fewer women list AI-related skills on LinkedIn than men. Whether this reflects actual workforce participation, differences in how people present their skills, or both, it points to a persistent and visible gender gap in the AI talent pipeline.

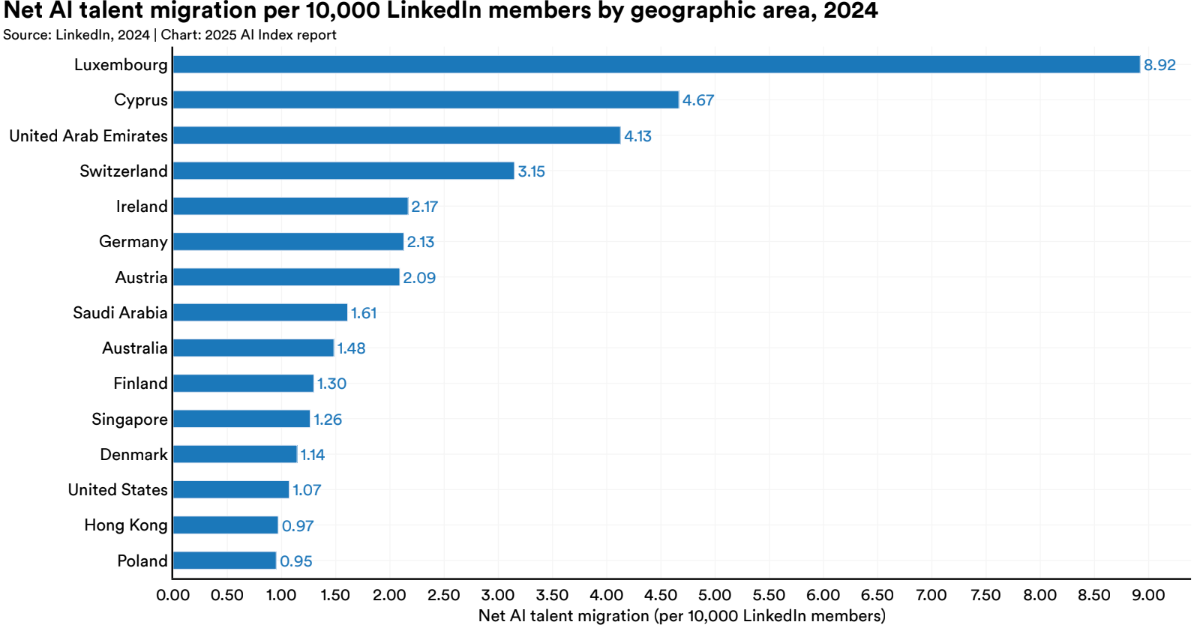

Talent on the Move

While AI skill disparities persist, AI professionals themselves are on the move, reshaping regional competitiveness. The countries attracting the most net AI talent per capita in 2024 were:

Luxembourg (+8.92 per 10,000 LinkedIn members). Cyprus (+4.67). United Arab Emirates (+4.13).

In contrast, traditional powerhouses like Canada and the Netherlands have seen talent inflows slow or even reverse over the last two years. Countries with rising ecosystems like Saudi Arabia are also starting to register real inbound flows.

The global AI job market is becoming less anchored in a few hubs.

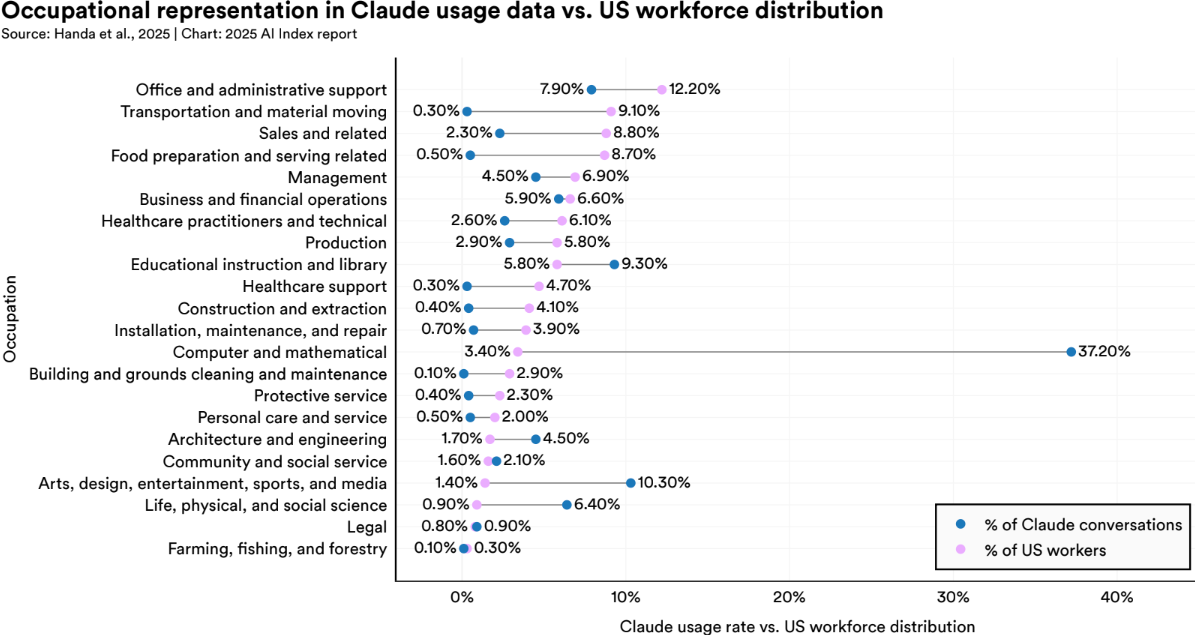

Who's Actually Using AI, and for What?

Anthropic's Claude usage data gives us rare insight into how generative AI is used across real job functions. The clear winner? Technical occupations. Over 37% of Claude's usage came from people in computer and mathematical roles, followed by creative sectors (10%) and education (9.3%).

Claude usage data shows that tasks fall into two broad categories:

Augmentation (57%): helping people think, write, summarize, and solve. Automation (43%): doing tasks independently.

2. Investment and Infrastructure

AI is also reshaping where capital flows, who builds the core infrastructure, and which players are positioning themselves to define the global AI stack.

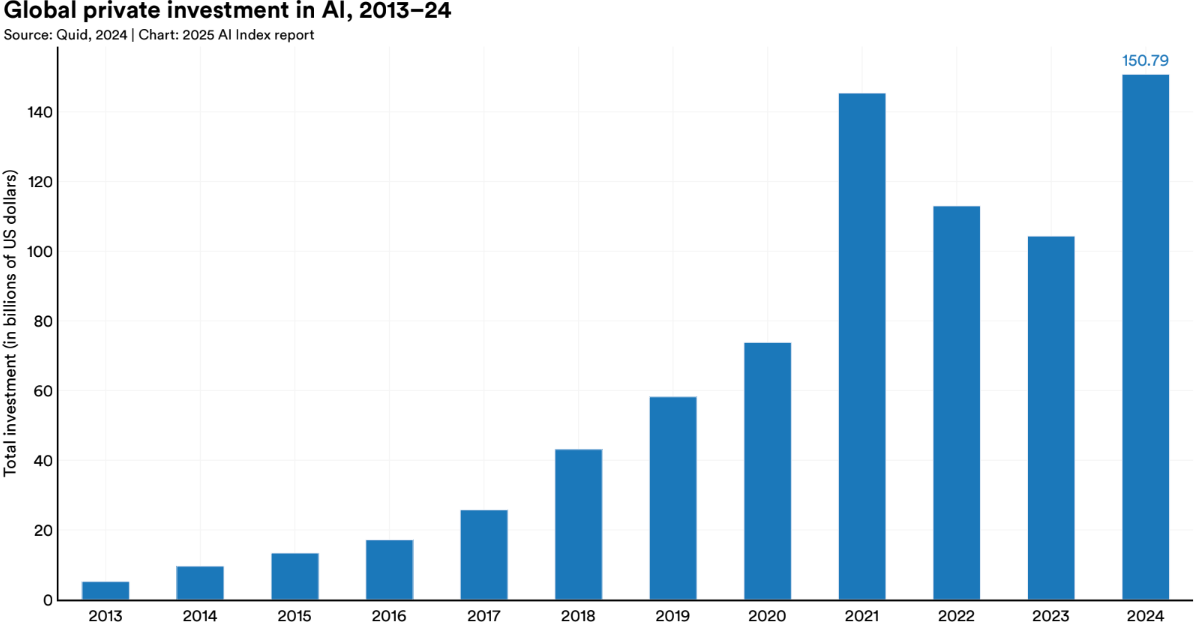

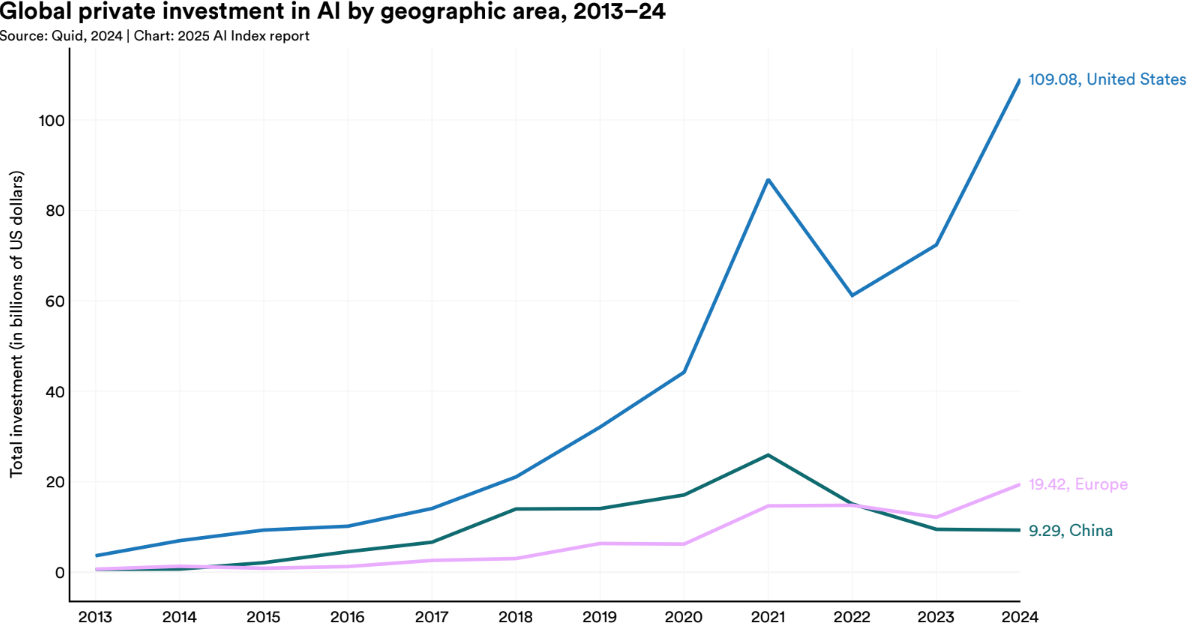

In 2024, global private investment in AI reached $151 billion, a nearly 50% jump from 2023. Of that, Generative AI alone accounted for $34 billion, or about +20% of total private investment.

While the U.S. still dominates, the geography of investment is shifting. Europe has now surpassed China in private AI investment for the first time, though it still trails the U.S. by a wide margin.

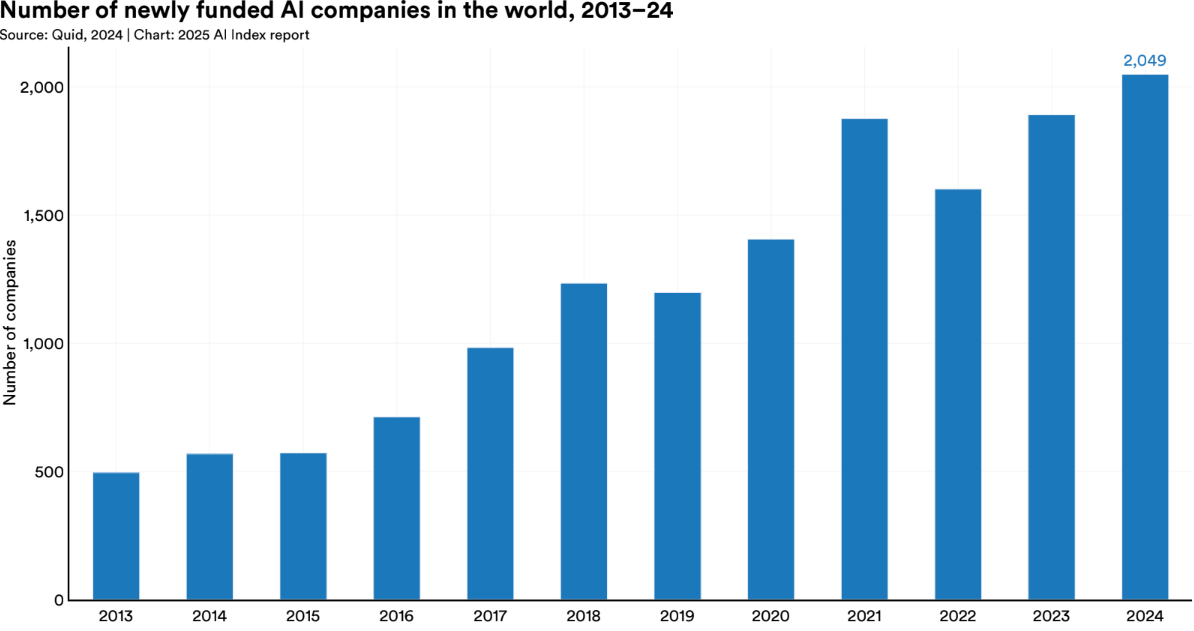

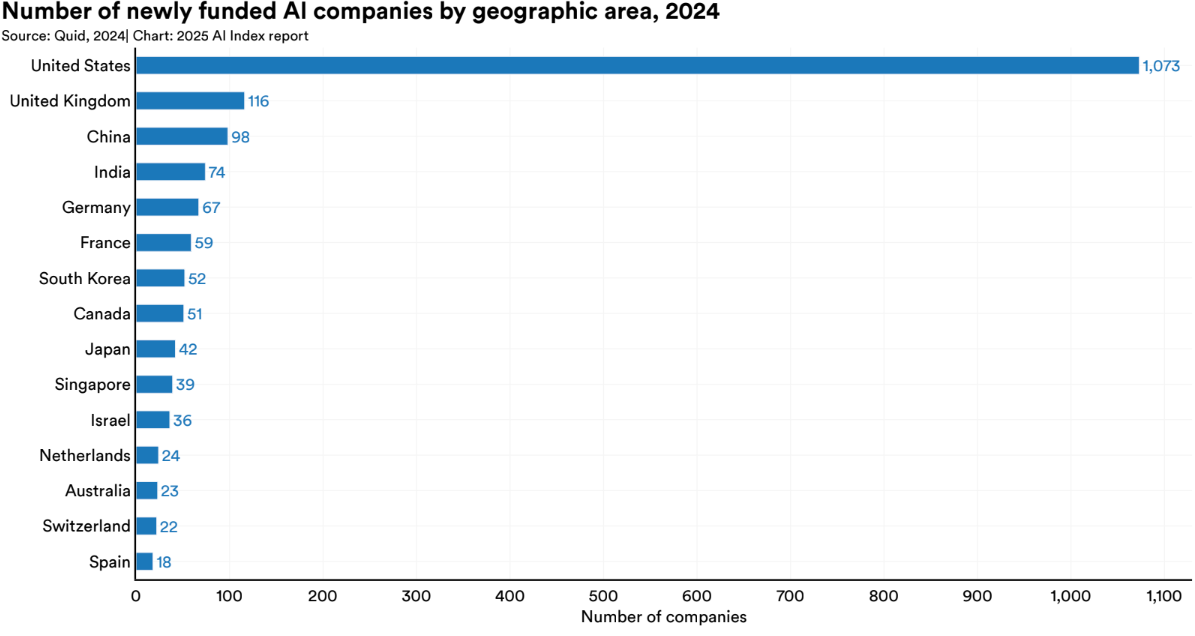

In terms of company count, over half of newly funded AI companies in 2024 were U.S.-based, followed by a growing number of startups in the U.K., France, and India.

The Top 5 AI Operations of 2024

Here are the five most valuable operations highlighted in the AI Index:

- Synopsys acquires Ansys for $35 billion: This acquisition bridges chip design and simulation, fortifying Synopsys' position at the foundation of the AI hardware and electronic design automation stack

- Databricks raises $10 billion: Specializing in enterprise-scale data infrastructure and AI-native platforms, Databricks' raise reflects investor confidence in AI tooling, not just models

- OpenAI raises $6.6 billion: The most watched name in generative AI continues to scale, with funding aimed at infrastructure expansion, model R&D, and platform integration

- xAI secures $6 billion: Elon Musk's AI venture entered the arena with a huge round, immediately becoming a contender in the foundation model race and compute power competition

- Amazon invests an additional $4 billion in Anthropic via AWS: More than a partnership, this deal deepens strategic alignment, embedding Claude models into the AWS ecosystem and scaling shared infrastructure

These are structural plays shaping who controls compute, who owns deployment, and who sets the pace for AI infrastructure at scale.

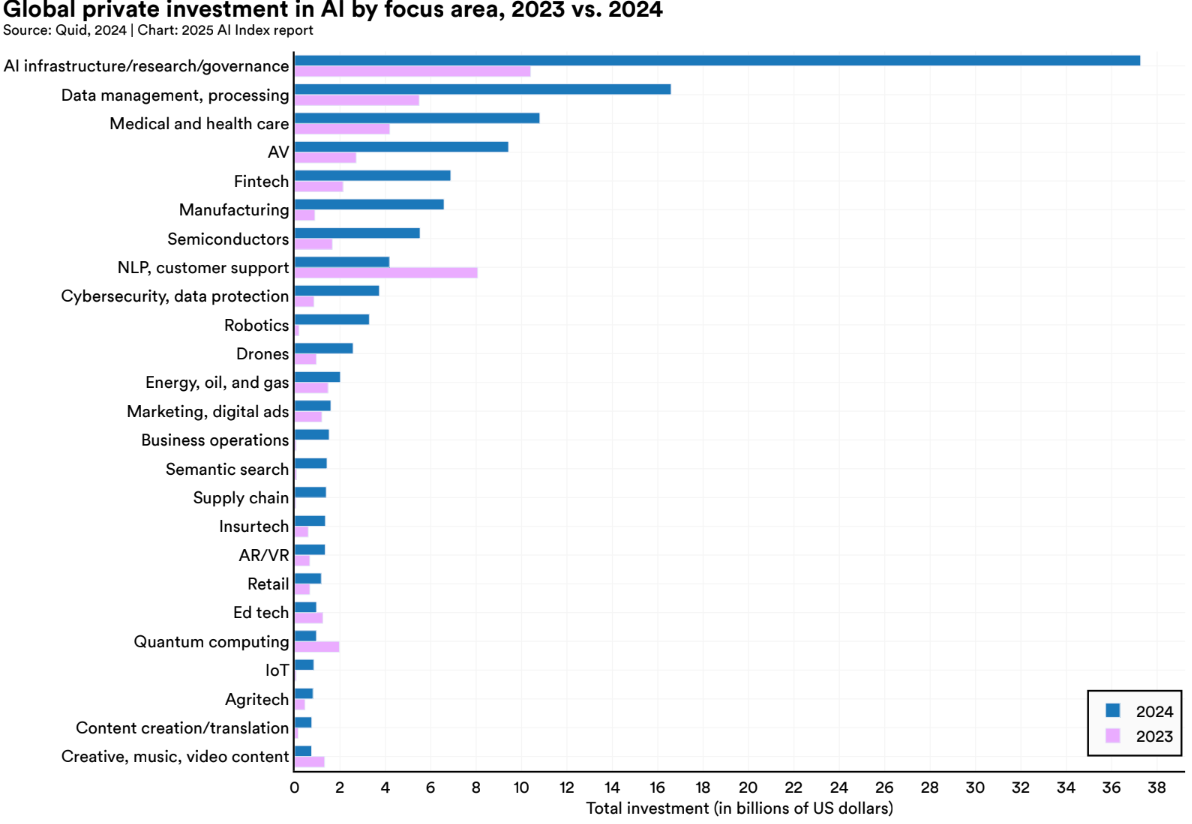

Where the Investment Is Going

The dominant focus areas in 2024 included:

Natural language processing. Computer vision. Model development. And increasingly, AI infrastructure, governance, and safety research.

Notably, AI infrastructure and governance saw the largest growth rate, signaling that investors are now paying attention to not just what models do, but how they scale safely, efficiently, and under policy scrutiny.

Governments Step In with Big Investments in 2025

Private capital still dominates the AI race, but public money is no longer on the sidelines. In early 2025, two major announcements signaled that governments aren't just regulating AI. They're starting to fund it like infrastructure.

In the United States, the "Stargate" initiative, a proposed $500 billion public-private AI infrastructure program, continues to take shape. Its goal? Secure long-term dominance in compute, chips, and national-scale model development.

In France, President Emmanuel Macron unveiled a €109 billion AI investment plan, backed by MGX (UAE) and Brookfield (Canada), focused on:

Building national AI infrastructure, including large-scale compute powered by low-carbon nuclear energy. Supporting sovereign model development and domestic AI companies like Mistral.

These moves mark a shift: AI is now a geopolitical strategy.

Conclusion

The 2025 AI Index shows an industry scaling fast, reshaping economies, workforces, and investment priorities. AI skills are no longer optional but embedded into hiring standards and organizational structures. Companies are restructuring entire departments, while billions flow into R&D, infrastructure, governance, and the raw power needed for industrial-scale AI.

The biggest players are consolidating. Governments are entering with serious capital commitments for technological sovereignty. Europe still lags the U.S. and China in scale but is no longer an afterthought. AI is also becoming an increasingly multi-polar race across North America, Europe, the Gulf, and Asia.

The future won't be decided by who builds the biggest model but by who builds the smartest ecosystems: talent, infrastructure, governance, and energy. The industrialization of intelligence is underway. If you're still thinking of AI as a side project, you're already behind.